4th and Long

By: Amir Bashir & Janek Boski

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

Arian Foster, running back for the Houston Texans NFL team, announced in late 2013 that he would be the first athlete to launch an initial public offering (IPO) of himself, giving up 20% of all future earnings for $10.55 million up front. Shortly after, San Francisco 49ers tight end, Vernon Davis, and Buffalo Bills quarterback, E.J. Manuel, both announced their own IPOs as well. These investment opportunities were announced in partnership with Fantex Inc., a newly formed market exchange that seeks to be the first trading platform where athletes can launch their IPOs. Fantex’s vision is that investors will dedicate capital towards creating a portfolio of athletes, similar to that of corporate stocks, as they seek to generate a return.

Here are the Stats

Fantex operates similarly to the New York Stock Exchange, but provides a much more integrated service by recruiting, valuing and marketing athletes to potential investors. Currently partnered with investment bank Stifel Nicolaus & Company, Fantex has so far embarked on an IPO roadshow offering a stake in the future income of selected NFL players to investors through a tracking stock. The trade-off is as follows: the athletes receive an upfront payment in exchange for a set percentage of their future earnings. Fantex collects 5% of the income from these earnings to fund their platform stock, which is essentially an exchange trade fund (ETF) with a small stake in all players ‘brands’ that Fantex represents. On top of capital gains generated from trading players’ stock, investors are periodically distributed a dividend at the company’s discretion. Fantex controls all fund disbursements, much like a public company would control the movement of excess income to its shareholders. This process continues until Fantex decides to convert the investors’ tracking stock into shares of Fantex Inc. platform stock. This occurs when Fantex’s board initiates the conversion under ‘good faith’, due to player retirement or a material event resulting in the likely decline in the athlete’s income. With this integrated structure, investors are not only speculating on the success of the athlete, but also on Fantex’s operations, as they will have a stake in the company if they keep their investments for long enough .

Fantex’s revenue model is also based on the volume of transactions on the platform. Fantex charges a 1% fee on the total value of trades, compared to the NYSE which makes $0.003 per 100 blocks of shares traded on the exchange. To illustrate this model, if 1000 shares of Arian Foster traded at $10 on the Fantex platform, the company would generate $100 in fees, while the same trade on the NYSE would yield just three cents.

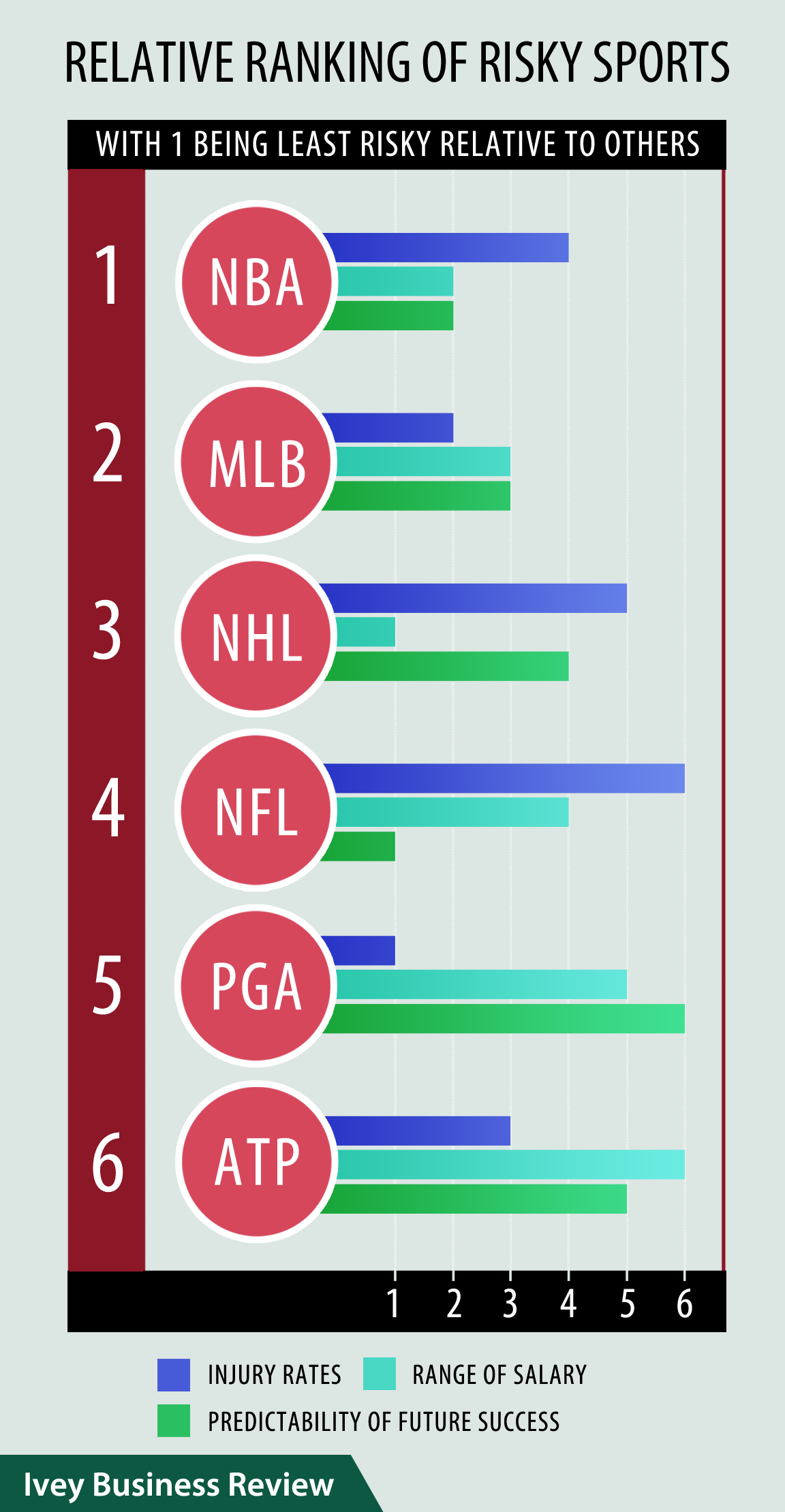

An Injury Waiting to Happen

Fantex’s current strategy is to appeal to emotional investors by targeting high profile players in order to provide the necessary demand to stimulate trading and build the size of the platform. However, picking investments based on emotional decisions has the potential to inflate players’ valuations beyond their intrinsic value, creating an unsustainable bubble that could potentially burst. To ensure this risk is mitigated, Fantex should focus on tailoring its future offerings to sophisticated investor demands.

Fantex should create a larger breadth of options to its investors through offering a diverse set of investment vehicles, an attractive array of athletes from different sports, and a diversified range of athletic skill levels. With its current common stock offering, Fantex’s investment vehicles are comparable to traditional equity, with a set convertible feature when the underlying asset loses its value. In other words, when the athletes’ ability to generate income declines, the associated tracking stock becomes worthless. With the risk of fast depreciation in the event of an injury or underperformance, Fantex should adopt multiple investment platforms that entice investors looking for a lower risk investment in athletes.

Diversify Athletic Investment

To enhance the investment appeal, Fantex should offer various security structures, such as those that resemble debt. These securities would function like a convertible debenture in which investors provide a lump sum to athletes and then receive periodic interest payments in return, while having the option to convert the security to equity and realize a stronger return should an athlete outperform expectations. This structure also has the flexibility to include debt covenants, restricting the use of the proceeds to appropriate uses such as training costs and brand development. Just like the current stock structure, Fantex would facilitate the contract and flow of payments thus receiving a 1% fee on the transaction value.

Expand the Sports Network

Diversifying the sports it offers is another way Fantex can develop the full risk spectrum of its platform. While Fantex’s preliminary focus on football will drive demand, it is a risky sport to invest in due to high injury rates, short careers, and a plethora of players. Analysing the injury rate, the salary range, and the predictability of future success, MLB (baseball) and the NBA (basketball) have been identified to have the lowest volatility, suggesting that these sports could be an alternate low risk option for investors. On the other hand, the ATP (tennis), PGA (golf) and NFL offer the most risk due to their unpredictability of success. In the short term, focusing on low risk sports such as baseball and basketball would afford Fantex a proof of concept, while covering sports across a wide range of risk categories should be the eventual goal.

From All-Stars to Rookies

The last step in providing Fantex investors with true diversification options involves building out a wide range of athlete skill levels that range from the promising rookie to the established elite athlete. Fantex has already begun targeting big name athletes such as Arian Foster and Vernon Davis, yet a focus on younger up-and-coming players may be more valuable to Fantex’s investor base.

After compiling data from the 1995-2010 NFL, NBA, and MLB seasons, a study looked to see whether the draft position of a player was correlated with him becoming an All-Star (the study identified elite players as those which were selected as All-Stars during their careers). In most cases there was no evidence to suggest that the first draft pick was more likely to become elite than the 10th. Though this pattern may not continue in the long-term, it does suggest that draft order is not as significantly related to achieving elite status. Since #6-10 draft picks are no less likely to become elite players as the #1-5 picks, yet do not receive the same performance hype, they can be seen as undervalued. This same logic can be applied to young athletes that have been in the league for 2-3 years, were #6-10 draft picks, and have yet to realize their full potential. This undervaluation provides Fantex with more attractive investment opportunities to present to investors.

The Future of Sports Investments

First and foremost, Fantex needs to earn enough capital to fund the development of the proposed financial vehicles while proving to investors and the public that athletes can successfully IPO their future earnings into valuable stock offerings. As described above, allowing baseball players to “go public”, offers a lower risk option to investors and thus is a logical first step. When Fantex’s entire earnings boil down to a handful of contracts, losing any player to injury is dangerous, with baseball offering a chance to minimize this risk. At the same time, as America’s favourite pastime, baseball has a strong following and passionate fan base – the perfect short-term target market for Fantex.

IPOing baseball stars, such as Jose Bautista of the Toronto Blue Jays, would accomplish three key goals. First, it would show the public that these IPOs can in fact boast stable functionality. Building public plausibility serves Fantex by promoting to the next round of investors – those who may have been too timid for the first IPOs to hit the market. In addition, more athletes would be open to following the IPO route should they see their teammates successfully complete the process. This will generate a greater supply of athletes to IPO and greater demand for their public offerings from the public. Adding to this mix will be the media buzz surrounding the IPO activity. The more athletes that Fantex offers, the larger the buzz, and the more momentum the company can swing into the next round of IPOs. Most of all, the successful IPOs of a highly paid athlete will generate strong revenue for Fantex through trading and brand income collection. When Fantex finds itself with a cash surplus and a steady state of income, it will be ready to progress onto creating and installing the new investment vehicles tailored for investors with lower risk appetites.

In the anticipation of the inevitable second wave of investors – those who applaud the novelty of public athletes, but are suspicious of the security of the investment – Fantex should next develop its debt-like instruments. Like before, Fantex needs to target low-risk players to back these financial instruments. However, this isn’t to protect Fantex, but rather the investors who act as the creditors. Essentially, Fantex should continue to target the same players as before, but begin structuring these new contracts as convertible debentures. In doing so, Fantex will be adding some of the required variation in financial instruments, while still limiting the risk it exposes itself to. It is important to note that most of these vehicles will be released on the same athletes. For example, a convertible debenture will require an athlete has tracking stocks to convert to. Therefore, low risk players will start having public offerings with both debt-like and equity like investments tied to them.

As investors witness the deployment of both the debt-like instruments and the success of the original equity-like investments, it will be important for Fantex to maintain a steady state with its operations. Moving too quickly may incite fears of a bubble, driving investors away from the firm. Rather, Fantex should allow these debt and equity investments adjust to the market and reach a normal equilibrium. For investors, the most powerful thing Fantex can do to convey the legitimacy of the financial vehicles is to live and grow on their own, demonstrating the validity of their structure.

Finally, as investors and the public in general become more accepting and relaxed with the idea of investing in athletes, Fantex can release the final portion of the proposed financial vehicles. By rolling out the offering of select financial vehicles, Fantex will have created a risk spectrum – a truly differentiated market based on sports figures with varying levels of risk for the large majority of investors.

Investing in athletes is inherently riskier than a corporate investment. Inevitably, athletes will decrease their earnings potential and can swiftly move to the sidelines given an injury, attracting the spectrum of high risk investors to Fantex Ultimately, these innovative financial instruments – like Arian Foster and Vernon Davis – would one day find themselves residing amongst a portfolio of stocks like Apple, MasterCard, and Bank of America.