LafargeHolcim: The Plastic Solution to the Global Sand Wars

By: Joseph Scarfone

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

Shifting Sands

You might be surprised to learn that sand is the world’s most commercially consumed solid natural resource. The United Nations estimates that sand accounts for 68 to 85 per cent of all solid resources extracted from the Earth and as demand for the material continues to rise, this trend is expected to continue. The natural resource is finite, however, and experts broadly agree that sand’s scarceness is quickly becoming a crisis.

Upwards pressure on sand prices is already apparent. Singapore, for example, has seen sand’s price climb from €2.5 per metric ton to a staggering €161 per metric ton over the past 40 years. As prices increase, heavy consumers of the raw material face increasing headwinds, with the global construction industry particularly affected. Sand makes up 80 per cent of concrete and 94 per cent of asphalt, in addition to being the base used in construction projects. As demand continues to grow in light of dwindling supply, companies that can reduce their long-term reliance on this resource will enjoy an advantage over those who cannot.

World Industrial Silica Sand Demand

Source: The Freedonia Group

A Supply Chain Built on Sand

LafargeHolcim, based in Switzerland, is the largest cement producer by installed capacity. Its global presence spans over 80 countries, where it maintains a top three position in 80 per cent of its markets. Given the importance of sand to LafargeHolcim’s business model, controlling its exposure to this commodity is crucial.

LafargeHolcim already faces the challenges inherent in procuring large volumes of a scarce commodity. In 2018, the company was charged with allegedly supporting ISIS through terrorist financing to keep its Syrian operations running. These charges are especially problematic for LafargeHolcim as a substantial portion of its shareholder base consists of parties sensitive to environmental, social and governance (ESG) principles. In 2016, Aslak Skancke, a member of Norway’s public pension fund’s ethics council, acknowledged it would “be problematic if a company we have investments in paid money to ISIS to maintain its operations”; as of November 2018, the fund continued to hold a stake in LafargeHolcim. To simplify operations, restore its reputation, and regain confidence from its shareholders, LafargeHolcim must find a sustainable solution to its supply chain troubles.

The Global Sand Crisis

Despite apparent widespread availability around the world in areas such as the Sahara Desert, not all sand is created equal. Only sand of a certain grade, known as aggregate grade, is useful for commercial use, and aggregate sand is in short supply. In many regions of the world, traditional sand mines have already been depleted or decommissioned. As these supply sources dwindle, unorthodox methods such as collecting sand from the ocean floor are increasingly used. In addition to harming coral reef ecosystems, this type of aggregate is undesirable as it contains a high salt concentration and requires treatment before it can be used.

In response, illegal supply is playing an increasingly important role in the global sand trade. In India alone, the value of illegal sand mining is conservatively estimated at $250 million. These markets, however, have been widely implicated in political corruption, violence, and even murder. Given the ESG values held by LafargeHolcim’s shareholders, these ethical concerns supersede any possible economic benefit that could be realized.

Demand for sand is equally as complex. The commodity is a critical component of numerous finished goods ranging from glass, to electronics, to artificial islands off the Chinese and Gulf coasts. However, sand is the primary component of concrete, cement, and asphalt, which collectively account for the largest use of the resource. Considering unprecedented urban development in underdeveloped regions across areas such as Asia and Africa, the demand for sand has never been greater. Between 2011 and 2013 alone, China used more sand than the United States used in the entire twentieth century. Sand is integral to construction, which is necessary for global economic development.

Strategic Alternatives

Given finite supply and growing demand, the price of sand seems constrained to rise in the long term. LafargeHolcim already operates a significant number of sand mining sites across the world, but the supply of new sand mines is drying up. It could continue to use increasingly environmentally unfavourable means of extracting sand internally or rely on actors with questionable human rights records, but neither action serves as a long-term solution.

Fortunately for LafargeHolcim, the answer might lie in a different material altogether: new research indicates that there are alternatives to sand acting as an input in aggregate. A University of Bath study published in February 2018 concluded that 10 per cent of sand in concrete can be safely replaced with recycled plastic without substantially compromising structural integrity. This groundbreaking research, awarded the Atlas Award in recognition of its potential societal impact, shows LafargeHolcim a way forward.

Paving the Way for Success

Roads and highways can be built with asphalt or concrete. Since as early as 2001, Dr. Rajagopalan Vasudevan, a chemistry professor in India, has been a leader in advocating for the use of waste plastic as an input in asphalt roads. In addition to reducing the quantity of bitumen required by six to eight per cent, plastic-modified roads have been shown to have an increased lifespan. Using Dr. Vasudevan’s methods, Tamil Nadu, a state in India, constructed over 1,000 kilometers of asphalt road by incorporating more than 1,600 metric tons of plastic waste.

The University of Bath concrete study concluded that while its 10-per-cent plastic composite mix showed promise, it could not be used for structural applications, like the construction of a building, without further research.

Fortunately for LafargeHolcim, concrete used in roads has very different requirements than the kind used for constructing buildings. The Ontario Provincial Standards for Roads and Public Works stipulates that high strength concrete is defined by its compressive strength of 35 MPa, while a Minnesota Department of Transportation study lists roadworthy concrete standards at 3,000 psi (20.7 MPa).

An existing study from University Bourmerdes in Algeria tested the strength of various concrete-plastic mixtures where up to 50 per cent of sand was replaced with plastic waste. While the material’s strength fell as more plastic was introduced to the mix, its compressive strength exceeded 35 MPa even as half of the sand was replaced by plastic. Combined with the University of Bath’s recent breakthrough in structural strength, LafargeHolcim should take advantage of these academic findings and translate them to real-world applications, substituting plastic for sand in road-building concrete where the sand crisis is most dire.

Strength of Plastic-Integrated Concrete

Source: Concrete and Building Materials

This advancement in technology comes at an opportune time: earlier this year, India’s federal government announced a planned investment of 6.9 trillion rupees ($97 billion) in 83,677 km of roads over the next five years. An even larger infrastructure network, the Belt and Road Initiative, will be developed over the next decade to connect Asia, Europe, and Africa; Fitch Ratings anticipates that this initiative will entail more than $900 billion in infrastructure spending. Given the prevalence of sand scarcity around the world, it is unclear how this positive shock in demand will impact the price of sand. LafargeHolcim’s ability to offer road concrete without a heavy reliance on sand would enable it to outperform its competitors. Additionally, numerous countries participating in the Belt and Road Initiative are among the world’s worst generators of plastic waste, meaning that LafargeHolcim’s plastic roads could have a positive social impact while making use of scrap materials where they are most plentiful.

The Material Benefits of Plastic

In order to quantify LafargeHolcim’s opportunity, India’s sand and plastic market dynamics must be understood. While manufactured sand, created by crushing rock and quarry stones, has become more prevalent in the country, supply has failed to keep pace with demand and the illegal sand market continues to thrive. As of September 2018, the Times of India estimated sand prices on India’s black market at 1,500 to 2,000 rupees per metric ton. This represents an astounding 150 per cent increase within a time period of less than a year, largely catalyzed by increased regulation and a ban on certain mining practices.

The plastic markets in India act as an informal economy creating supplementary incomes for the poor. In much of the country, rural workers individually collect waste plastic to sell to regional aggregators at an estimated price of 14,000 to 15,000 rupees per metric ton of polyethylene terephthalate (PET) plastic. This plastic is then sold at a markup to vendors and recyclers.

Process for Plastic Roads

These prices suggest that as a raw material, plastic is substantially costlier than sand. Rather than a reason why LafargeHolcim should not pursue the strategy of building plastic-concrete composite roads, the apparent uneconomical nature of this business can be seen as precisely the reason why LafargeHolcim should enter the industry. Absent any competition, the company has the resources to develop scale and establish a more resilient supply chain for recycled plastic, potentially gaining significant cost advantage in the long run. In late 2017, the Director of Vietnam’s Department of Construction Materials acknowledged that the country may well run out of sand by 2020; as a country poised to receive significant Belt and Road Initiative infrastructure investment, it is quite possible other concrete manufacturers will be unable to satisfy construction demand. By entering this business when other players are prevented from participating, LafargeHolcim will gain a first mover advantage and streamline its operations, positioning the company to take full advantage of the Belt and Road Initiative.

Furthermore, sand’s current price does not reflect its future trajectory. The substantial jump in black market prices over the past year evidences the upward price pressure that is likely to continue. While it is difficult to predict precisely how quickly underlying fundamentals will translate to an increase in price, a foothold in the market would serve LafargeHolcim well and enable the company to capture economic profit once it appears. Keeping in mind that sand has already reached a price of €161 a metric ton (13,000 rupees) in Singapore, the turning point may be closer than anticipated.

Laying the Foundation

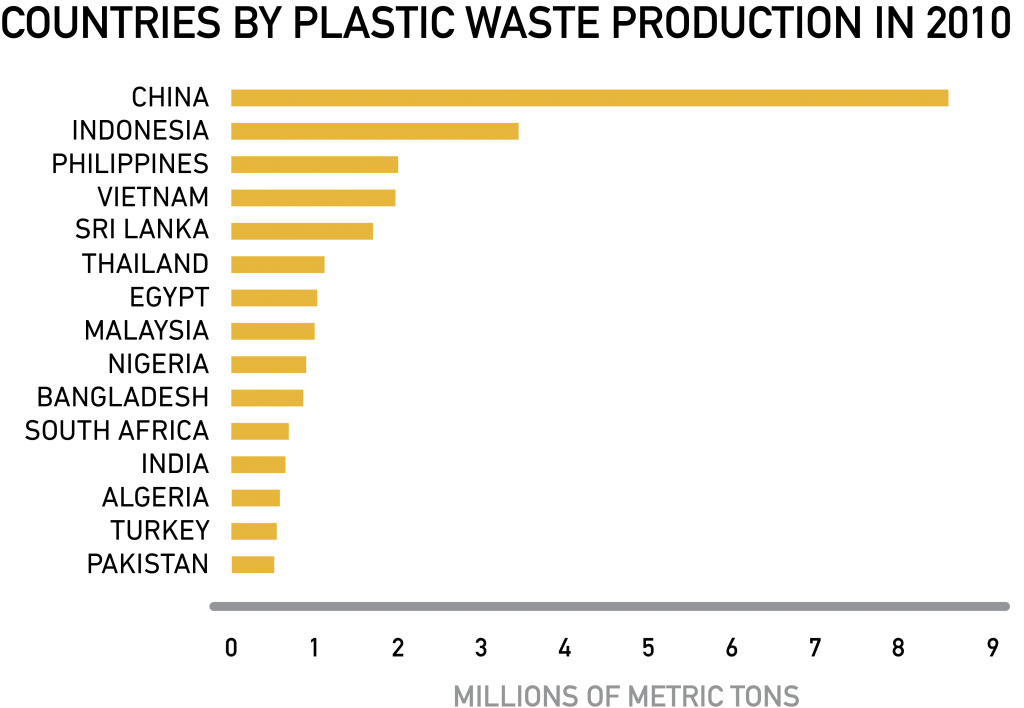

For years, Western countries, including the U.S., Germany, and the U.K., have exported plastic waste to China as a means of reducing buildup in domestic landfills. Since a ban was placed on this practice at the beginning of 2018, these countries are now seeking alternative outlets for their waste plastic. If LafargeHolcim can prove its responsible use of plastic, the company could feasibly source waste PET plastic at a substantially lower cost than the market.

Source: Science Magazine

To eventually sell its plastic roads in developed markets, LafargeHolcim should lobby governments to adopt more stringent road construction environmental standards. The public and government officials are likely unaware of the social, environmental, and economic costs of sand in their roads. Significant research and development would furthermore be necessary to ensure LafargeHolcim’s plastic concrete mix satisfies the rigorous safety standards of developed countries.

Within developing economies, LafargeHolcim should market the benefits of a more effective road network and reduced plastic waste, which align well with governments’ development priorities. In the long run, as the price of sand increases, this strategy will position LafargeHolcim to enjoy success surpassing that of its competitors.

Concrete Roads Ahead

As an increasingly scarce natural resource, sand’s price is poised to continue rising. In response, LafargeHolcim can combine its resources with new advancements in technology to secure a market-leading position in the nascent plastic road industry. Not only would this prove beneficial for the company, it would also benefit the environment by making use of waste plastic. The consequent positive environmental and social change would reiterate LafargeHolcim’s commitment to its shareholders and their ESG values, leading to a brighter future for all involved.