Uprooting an Entrenched Banking System

By: Kaitlyn Oh

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

With the rise of Netflix, Amazon, and Uber disrupting the media, retail, and taxi industries, the inconvenient truth is that banking is next on the horizon. With the rise of financial technology (FinTech) start-ups, Canadian banks could lose up to 60% of their retail banking and wealth management profits in the next decade. With retail banking accounting for anywhere from 50% to 70% of the Big Six Canadian banks’ profits, the overall hit could be as drastic as a 42% decrease in their bottom line.

With low risk tolerance and product-focused business models, the Canadian banks are moving slowly in a time of turbulence with a greater focus on what they are selling rather than on how they are selling it. While some banks have invested into digital labs and mobile apps, these efforts have been marginal and still maintain the focus on products as opposed to innovation. With a product- focused approach, banks risk being disintermediated as start-ups accomplish the same tasks of transacting, depositing, and exchanging funds with greater speed and convenience. With the number of FinTech start-ups globally now estimated at 12,000 and the investment into these firms growing exponentially at over 100%, these firms pose a significant threat to the banks’ traditional business models.

Drawing the Situation

Major threats are coming from all directions: lending, savings, and payments. The number of card products from alternative financial institutions, for example, PC Financial, Walmart, that are growing within consumers’ wallets is resulting in lower credit card revenues for banks, particularly with increased interest in digital banking, for example, Tangerine, Zenbanx; and alternatives to foreign exchange, for example Transferwise.

The payments segment, comprising 35% of banks’ profits and having experienced minimal disruption in the past 30 years, is particularly ripe for disturbance. With a growing number of new entrants, like Google Wallet and Apple Pay, the payments industry is inevitably undergoing an overhaul in its infrastructure, both domestically and for cross-border transactions.

In addition to threatening banks’ revenue sources, new payment solutions are also jeopardizing the banks’ access to customer data, a key source of competitive advantage over start-ups. As disruptor-facilitated payments run through independent systems, the information is scrubbed, leaving only the trace of the time and amount of the transaction. Without this transaction data, the banks are at a significant disadvantage when cross- selling and marketing their products. As products-based companies, without knowing which products to sell, the banks’ business model is at stake.

Options for Change

Faced with the need for a plan of attack, the banks have three available options. One option is for banks to develop in-house capabilities to rival start-ups. With app development costs ranging from a meager $50,000 to $150,000 and taking approximately 10 weeks, in-house development seems like a formidable idea. However, the Canadian banks have a poor history of in-house attempts. CIBC attempted to launch a mobile wallet that encountered low adoption rates and an Android app rated 2.5 stars out of 5. Similarly, RBC has sunk millions of dollars into projects facing similar results or never having made it to market.

The other option could be to provide a platform for Application Program Interface (API) or outsource payment services to other companies. However, both of these options provide the banks with little ownership and control in the development and future of the industry, and instead relegates them to a back-end role.

The third and most promising option is for banks to act as industry collaborators. Surveys indicate that more than 40% of banking CEOs view joint ventures, strategic alliances, and informal collaborations as the greatest opportunity for innovation and progress. In a study conducted by Deloitte UK, the collaboration option emerged as the clear preference for payments experts.

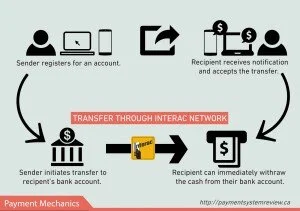

Leveraging the Network

Understanding that industry collaboration is the path most likely to be supported by CEOs of the Canadian banks, the banks need to turn to Interac – an avenue that would allow them all to succeed. The payment network holds the largest percentage of total number of transactions and is top-of-wallet for most Canadian consumers. It has national coverage and a 55% market share of the total transaction volume in 2012. With 9 out of 14 seats on the Board of Directors dedicated to the Canadian financial institutions, the banks have a vested interest and a great amount of control over Interac.

In the payment space, the Canadian banks and the start-ups specializing in payments can create a mutually beneficial relationship, where the banks can avoid previous failures of in-house developments and start-ups can reduce their financial risks on handling potential fraudulent transactions. Facing ever-growing threats and a tight timeline to develop in-house, Interac could act as a white-label network to facilitate peer-to-peer (P2P) payments for new financial institution related start ups, for example, Venmo, Popmoney and Chillr. It can provide an easy point of entry into the Canadian market place for the start-ups, acting as the network to facilitate the movement of funds, and charge the start-ups for the use of the payment network on a per transaction basis. In return, these new start-ups would allow Canadian banks to target millennial customers. Millennial customers have a longer customer life value since they are likely to still stay with traditional financial institutions as they grow older.

Start-ups would provide the user interface and technology backbone for any new apps and functionality; whereas the funds would be tied directly to customers’ bank accounts. Many start-ups already have the capabilities to provide the technology backbone an investment of only $50,000 to $150,000 to develop the mobile app. Start-ups should be willing to collaborate with the banks since the convenience of having payments tied directly to one’s bank account is cited as a key pain point for P2P payments. Additionally, this model would save the start-ups the hassle of handling payments and the risk of carrying liability for any fraudulent transactions, as with the current Interac model. As a result of such partnerships, banks can offer joint banking solutions, thus adopting aspects of a digital bank without investing large amounts of capital and undertaking the risk in developing these types of solutions. This mutually beneficial arrangement would allow banks to move towards digitization and take on lower risk while still appearing innovative and capturing young consumers.

With a similar approach taken by the Indian bank, HDFC, and a new P2P start-up, Chillr, HDFC gained 50,000 app downloads in its first month of launch. Similarly, a Barclays bank in the UK launched Pingit in February 2012. Growing from a simple mobile P2P solution on all major mobile systems, the service generated £255M in transaction volume in two years. Pingit then reached over £1.2B in transactions the following year by registering over 48,000 merchants and launching “pay-by-mobile” functionality, permitting users to pay at point of sale terminals using mobile. The app experienced 1.5x growth in transaction volume in each year of operations, proving to be a great case study for the Canadian banks.

Benefits to Start-Ups

Interac could provide a solution for start-ups to tap into the Canadian banking system. Already proven to be secure and established, Interac adds credibility to any Fin Tech start-up through its brand. Customers are demanding: two-thirds of Canadians are hesitant to trust anyone other than an established financial institution for making payments and 61% cite security as a major concern with mobile payments. As a burgeoning FinTech start-up, it is unlikely that a young company would be able to develop the level of trust necessary to overcome this inertia. In this manner, Interac could lend credibility to new start-ups and provide the support necessary to ensure greater traction and overcome some of these barriers to entry in the mind of the consumer. Additionally, the alternative for these start-ups to run payments is through a proprietary network, similar to PayPal. These closed- loop networks, which cut out intermediaries such as financial institutions, tend to be inconvenient and costly. It requires users to wait 1 to 3 days to cash out their funds and pay approximately 2.5% on the amount withdrawn.

This solution addresses more than just the consumer preferences; it also provides an easy way for start-ups to enter the Canadian market without going through the legalities of registering as a financial institution. The payments industry is heavily regulated within Canada, and to plug into the Interac network, companies need to be certified as financial institutions. This certification requires over $5M in paid-in capital, deep pockets, and the ability to accept deposits in addition to compliance with the 764-page Bank Act. This solution provides start-ups with a quick and easy way to enter the payment space, avoiding some of the regulatory restrictions around payments.

Short-Sighted Solution

The solution will only work in the short-term. Once the start-ups reach critical mass and can support their own infrastructure, the banks would have enabled one of their biggest threats, acting as the support to the f ledgling start- ups. In the current proposed solution, the only aspects that would retain the start-ups on a long-term basis would be Interac’s low pricing model. If the now-mature start-ups had deep pockets enabled by years of transacting through Interac and support from the Big Six banks, the start-ups could easily abandon the banks and take their user base with them.

The banks could pursue a number of tactics to retain these partnerships in the long-term. The first option would be to pursue acquisitions in lieu of partnerships; however, this option forces the banks to take on the risk of dropping large amounts of capital on unproven solutions. Another option could be for the banks to build contracts and force the start-ups into partnerships by making this the only way for start-ups to get access to the network initially. However, this option does not have a long-term view and contracts may eventually expire.

A third option available to the banks could be to co-brand the start-up solutions to ensure that the Interac brand name is propagated amongst consumers, similar to the way that MasterCard and Visa have become synonymous with credit cards. Through a co-branded effort, start-ups would still reap the benefits of Interac’s infrastructure, but Interac would also gain exposure to direct consumers. While this brand is established through the co-brands, Interac and the Canadian banks could begin developing their own in-house payment solutions. With the launch of these new in-house payment solutions, they could begin to gradually phase out and move users to their own proprietary solution without relying on the start-ups any longer. With a strong presence among its customers through the co-branding strategy, Interac has hope to help the Canadian banks retain the customers which were rightfully theirs.