Bunge Needs an Input

By: Tim Brady

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

Bunge Limited is a global agribusiness and food company that buys, stores, transports, processes, and sells various agricultural commodities. In 2013, the company operated in over 40 countries around the world and earned revenues of $61B. Bunge operates in five reportable segments, of which agribusiness is the largest, comprising approximately 75% of the company’s aggregate revenue. The company’s agribusiness segment is a leading global oilseed, vegetable oil, and protein meal producer with production assets in North and South America, Europe, and Asia. Historically, this segment has principally sourced and processed soybeans, rapeseed, and canola.

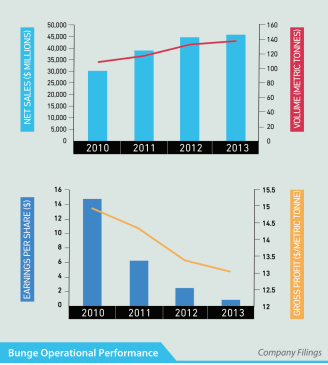

Of late, Bunge’s operating results have been directly affected by ongoing transportation issues and volatile commodity prices that have inhibited the company’s access to inputs. As a result, Bunge’s agribusiness has experienced a 43% year over year decrease in net income and the overall company has seen its EPS fall from $6.23 USD in 2011 to $0.90 in 2013. If Bunge is to combat the pernicious effects of sourcing and transportation risk that continue to plague margins in its agribusiness segment, the company will need to solidify its access to commodities. Furthermore, given the inherent commodity price risk prevalent in Bunge’s business, any alternative the company pursues should ensure it is purchasing raw materials at favorable prices and minimizing their commodity risk exposure.

(Agri)Cuture-Shock

Recent market dynamics have had dramatic adverse effects on the operations of crop processors. Consecutive record soybean and corn crops in the United States have resulted in oversupply, significantly hindering the agribusiness industry at large. The oversupply of soybeans and corn coupled with transportation bottlenecks has led to large inventories, resulting in significantly strained cash-flow conversion for farmers. Furthermore, the surplus of soybeans has caused prices to decline to $1,040 from a high of over $1,500 this year, eroding farmers’ profitability. This has made farmers hesitant to monetize their crop, contributing to the significant supply-side pressure the sub-industry is facing.

These problems extend beyond the United States, as other international sources of soybeans are also reluctant to export crops. Argentinian farmers, who collectively represent the third largest exporter of soybeans, are beginning to hold onto their crop to offset the rapid inflation prevalent in the country. This illiquidity has restricted Bunge’s access to key raw materials and has negatively affected the agribusiness’ bottom line. If Bunge is to better position itself to be profitable despite these systemic risks, it will need to find a way to guarantee access to affordable raw materials in order to improve throughput and capacity utilization.

The most obvious option to combat the issues of supply and price risk in commodities would be to purchase forwards. However, forward contracts offer no upside in yield, and often possess unfavorable terms. Rather than speculate on commodity prices through the use of derivatives, Bunge can employ a strategy that has been commonplace in the mining industry for decades – streaming contracts.

Streaming 101

Streaming contracts are an alternative form of financing in which the lender holds the option to buy a portion of the borrower’s assets as they are produced over time. The lender will deploy a majority of the capital at the beginning of the contract, with the remaining funds being paid as assets are delivered. These alternative lenders offer a form of non-dilutive financing to companies without increasing its leverage. Historically, streaming contracts have been concentrated in the mining and oil and gas sectors, as they require significant amounts of upfront investment. Despite previous consolidation, streaming contracts are beginning to diversify, as new industries are demanding alternative financing options.

Recently, an innovative Canadian firm has sought to address the market imbalance and provide farmers with flexible financing. Input Capital is the first agricultural streaming company and has entered into canola streaming contracts with 21 farmers to date. Input deploys capital to canola farmers in exchange for future crops at a fixed, discounted price over a six-year contract. Furthermore, farmers are provided access to an agrologist to help grow the best possible crop. For the lender, this arrangement offers guaranteed crops with the option for additional rewards when a farm performs exceptionally, in exchange for providing upfront capital to farmers. Moreover, the flexible nature of the financing allows farmers to better navigate their capital requirements, lower costs, improve efficiency, and capitalize on changing market conditions without being restrained by burdensome covenants typical of bank debt.

Notwithstanding its initial success and future potential, Input does not possess the necessary scale and financing to enact market change or consolidate a significant portion of the industry. The company’s market capitalization is less than $200M, while it current contracts represent 0.19% of the canola market in Western Canada alone. With additional scale and financing, not only would Input Capital be able to continue to unlock value in the canola market, but it would also have the capacity to expand this business model to other crops and other geographies.

Capital-izing on Vertical Integration

In order to combat its recent sourcing calamities, Bunge should pursue an acquisition of Input Capital. Despite Input Capital’s expected receivables of canola currently representing an insignificant percentage of the tonnage required for Bunge’s agribusiness, Input provides Bunge with an extensive business platform to utilize for potential growth. While Bunge could choose to replicate Input’s business model without making an acquisition, this type of venture is far removed from Bunge’s core competencies. Input Capital’s management expertise and history of success in agricultural finance are significant advantages to the proposed acquisition. Furthermore, this new business model could revolutionize Bunge’s raw material sourcing, solving a problem that has plagued the company for years. The most valuable assets that acquiring Input Capital would provide Bunge is Doug Emsley and Brad Farquhar, Input’s CEO and CFO. Doug Emsley and Brad Farquhar were both founding partners of Assiniboia Farmland LP, a fund that owned wheat, barley, and canola producing farms in Saskatchewan. Assiniboia was sold to the Canadian Pension Plan Investment Board in 2013 after generating over a 19% annual IRR since 2005. Moreover, John Budreski, a special advisor to Input, is a director of Alaris Royalty Corp. and Sandstorm Gold Ltd, which both have similar business models to Input’s and have returned over 300% and 150% to shareholders since inception, respectively. Their collective expertise in agribusiness and alternative financing will help Bunge to bridge the competency gap between its current agribusiness expertise and the expertise required to successfully operate an agriculturally focused alternative lending practice.

Input Cultivation

Bunge’s larger access to capital and cheaper financing alternatives would allow Input to scale rapidly beyond its current business, which amounts to 35,000-40,000 base tonnes contracted and $42.5M of deployed capital. Bunge has $742M of available cash and $4.4B of unused capacity in its credit facility. Furthermore, Bunge is in the process of trying to sell its Sugar & Bioenergy assets. Collectively, these assets have a book value of $2.0B and a replacement value of $3.0B and would significantly boost the company’s available capital that could be deployed through streaming contracts. Overall, Input Capital can help to unlock significant value to Bunge by limiting its commodity supply/ price risk and guaranteeing production capacity. With Bunge’s assets and financing, the company could utilize Input Capital’s business model to sustain its current input sources, diversify across multiple different crops, and expand into new markets.

An Input Problem

Through acquiring Input and integrating vertically, Bunge could fix its raw material costs over the lives of streaming contracts deployed, thereby substantially hedging the commodity risk inherent to the industry. Hedging its commodity exposure would provide Bunge with increased visibility for future costs, granting the company greater leadtime to react to market dynamics. Additionally, Bunge could greatly reduce its international operational risk by deploying capital into countries suffering from distressed credit markets. Currently, Bunge’s South American assets are responsible for 36% of its agribusiness production capacity. However, both Brazil and Argentina are suffering from market dynamics that are restricting Bunge’s performance.

In Argentina and Brazil, there are limited third-party financing sources available to farmers. Bunge currently provides financing to some of its farmers, but the advances are limited and far shorter in nature. As a result of these underdeveloped credit markets and prevailing industry dynamics, Bunge is currently experiencing the lowest level of forward selling of new crops in Brazil in years. Furthermore, despite the decline in agricultural commodity prices, Argentinian farmers are holding onto crops as a hedge against inflation and currency devaluation. Through Input Capital, Bunge would be able to alleviate its sourcing problems in South America by providing farmers with the capital they need via longer term streaming contracts. Deployed capital would fix Bunge’s raw material costs over the lives of the streaming contracts and would guarantee commodity sources, thereby optimizing capacity utilization and substantially hedging commodity risk. Moreover, the company could limit its exposure to spot or near spot supply markets and earn a strong return on capital.

The Stronger Final Input

Recent headwinds have dampened Bunge’s operating results, as the company cited increased transport costs and volatile commodity prices among the reasons for its underperformance. Integrating Input Capital into Bunge’s business would allow the company to secure future commodity inputs. This will ultimately help mitigate operational risk and decrease the impact of commodity price fluctuation, specifically in South American markets. All that the $13B agriculture giant needs is Input Capital – a $200M alternative lender.