Aimia: Loyal To A Fault

By: Harshith Baskar and Mark Krammer

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

Mayday

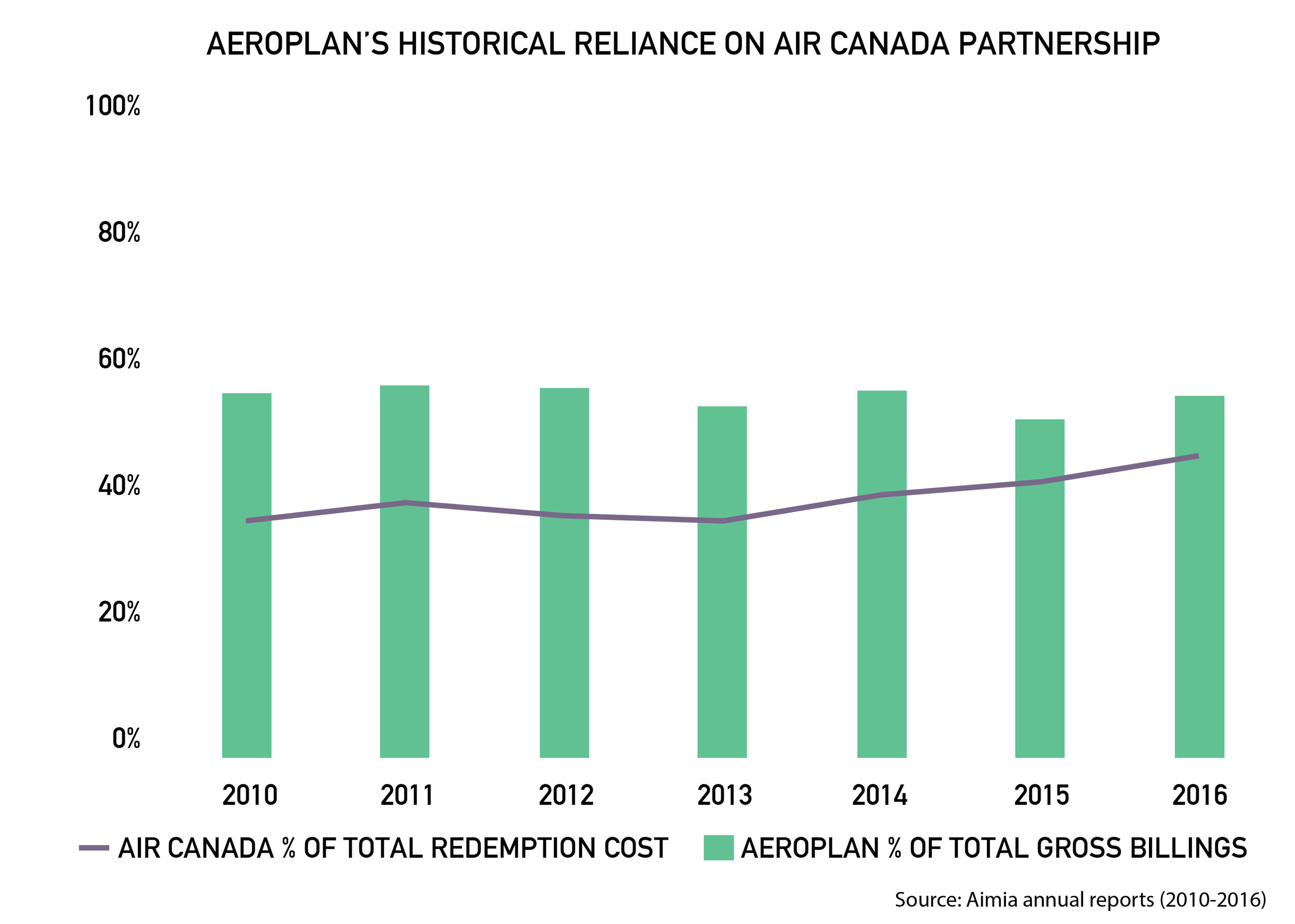

The Aimia and Air Canada partnership went awry this summer when the airline announced it would not be renewing its contract upon expiration in 2020. Instead, Air Canada plans to launch an internally-developed loyalty program. Markets were quick to respond, with Aimia’s share price falling more than 60 per cent the morning following this announcement. The evaporation of C$850 million in company value reflected the serious doubt cast on Aimia’s long-term viability. This dramatic value reduction came as no surprise given that each year, almost half of all Aeroplan member points are redeemed toward Air Canada seats.

Overexposure risk is a fickle topic: while securing a sizable contract from a single vendor can help the bottom line, such dependence can lead to disastrous consequences should the business relationship turn sour. Historically, Aimia has been a company with a track record of dependence on Air Canada. Of Aimia’s C$2.3 billion in gross billings over the last fiscal year, 57 per cent was derived from the Aeroplan coalition loyalty program. Due to Aeroplan’s network of various organizations, most of which are in non-competing business verticals, the program can provide customers with a greater variety of rewards and benefits than a traditional single-company loyalty program.

Turbulence and Tailspin

In years past, Aimia and Air Canada have enjoyed a mutually beneficial arrangement from the operation of the Aeroplan program. The airline purchased Aeroplan Miles from Aimia and in turn, Air Canada awarded loyalty points to its clients. Air Canada enjoyed the intangible benefits associated with participating in a recognized coalition loyalty program, including increased customer retention, cross-business promotion, and the possibility of gaining new customers. Over the past decade, this relationship proved beneficial to both companies as Aimia’s revenues grew to C$2.2 billion from C$709 million and Air Canada’s to C$14.6 billion from C$10.1 billion.

The severe impact of Air Canada’s decision to not renew its contract highlights a number of key strategic miscalculations made by Aimia over the years. Ever since the company’s inception in 2002, a sizable portion of Aimia’s income has been dependent on the performance of the Aeroplan program. The company has attempted several haphazard diversification efforts throughout its existence, but many were ultimately divested. In Aimia’s eyes, these divestitures were an opportunity to “focus on [its] core assets,” as stated by former CEO Rupert Duchesne. In reality, these efforts perpetuated Aimia’s heavy reliance on Air Canada with no recourse in the event of contract cancellation.

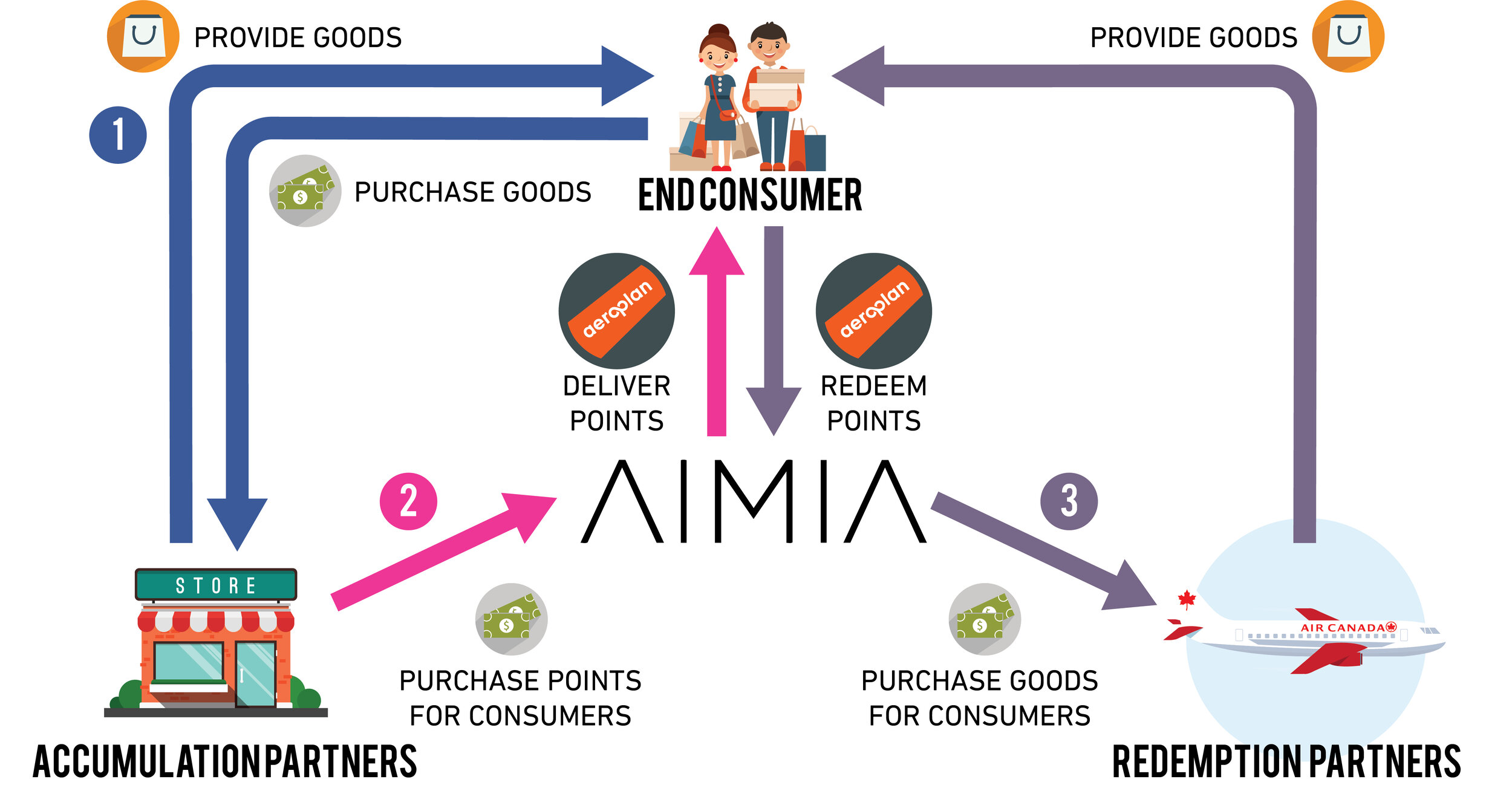

Aimia Ecosystem

The opportunity to outsource operations of a loyalty program was initially an effective value proposition to Air Canada. However, as Air Canada transitioned from a company on the brink of bankruptcy to the multi-billion-dollar behemoth it is today, its internal capabilities and brand also grew—eventually dwarfing Aeroplan in brand recognition. Furthermore, Air Canada’s two main domestic competitors, WestJet and Porter Airlines, both operate their own loyalty programs: WestJet Rewards and VIPorter. Compared to Aeroplan, these loyalty programs offer customers a streamlined experience when earning and redeeming rewards, providing the carrier increased control over the program. To Air Canada, the value encapsulated in Aimia’s services was no longer adequate to justify the cost of remaining a partner. Given the airline’s increased capabilities and competitive positioning, developing an internal loyalty program made strategic and operational sense.

The strong association between Aeroplan and Air Canada significantly impacted the perceived attractiveness of the coalition loyalty program following the airline’s exit. Aimia needs to leverage its expertise as a provider of travel services and its base of more than five million Aeroplan cardholders to dissociate itself from Air Canada and provide meaningful value to its customers and remaining partners.

Emergency Maneuvers

For the foreseeable future, Aimia cannot stop offering flights as a rewards option. Most redemptions are for travel-related services, and abandoning this offering would alienate consumers, reducing the company to one of many undifferentiated loyalty programs. Aeroplan will no longer have Air Canada as an exclusive partner nor will it receive preferential pricing. However, Aimia can still purchase airline seats as an independent third party, as has been done by its competitor, Air Miles. By establishing that Aeroplan points are still redeemable on flights after the contract expiration in 2020, the risk of a run on redemption is significantly reduced.

Aimia should facilitate the selection of lower-cost, non-air travel rewards and work to develop more diverse brand associations. Currently, a customer wishing to redeem rewards by calling the Aeroplan Contact Centre can only redeem points for airline seats, with all other rewards requiring online redemption. Going forward, Aimia should provide an integrated travel offering, ranging from different forms of transportation to tangential services like travel management, entirely through the Aeroplan Contact Centre. As a result, the end-consumer experience would be enhanced, and the risk of overexposure would be minimized.

Rather than viewing the obligation to offer travel-related services as a burden, Aimia should take advantage of its extensive experience in travel bookings and its relationships with hotels and vehicle rental companies. In fact, the company’s current service offering is not drastically different from that of a firm in the corporate travel management industry. This industry, in which a firm evaluates potential travel itineraries and books travel and accommodations on behalf of corporate clients, has been growing at a rapid pace. Providing an ancillary travel management service would increase the degree of partner interaction and streamline the purchasing and redemption processes, thus improving the chances of customer retention. It would also give Aimia more control over the reward redemption process, and would reduce the company’s overall redemption cost. This is because non-air rewards such as hotels and vehicle rentals, cost the company significantly less to redeem than their counterparts. This would also help reposition Aeroplan’s brand as an integrated travel rewards provider, given its existing relationships with many travel partners, including more than 30,000 hotels worldwide.

Adjusting Course

Historically, Aimia focused on targeting individuals as end consumers of its Aeroplan points program. To achieve long-term growth, Aimia must translate this expertise into strengthening its business-to-business (B2B) offering. Although Aeroplan currently partners with Amex Bank of Canada to offer a corporate credit card, this product has failed to gain widespread use and does not significantly contribute to revenues. Furthermore, the lack of commentary on this product’s past performance and future direction in Aimia’s latest annual report signals the company’s lack of focus on its B2B partners. The introduction of a parallel brand, carefully curated partners, and additional value-added services, including corporate travel management, would assist the company in capturing the B2B market.

The proposed Aeroplan Global Business Rewards program would target businesses as the end consumer of Aeroplan’s points system. Aimia can accomplish this by creating a new category of loyalty points, Aeroplan Business, with an expanded range of corporate partners. These new partners would be solicited based on their appeal to business customers and could include professional service firms, food and parcel delivery services, and travel-related services, such as existing hotel and vehicle rental partners. The opportunity allows Aimia to benefit from the C$5 billion business-related travel market and take advantage of high growth in industries such as the food delivery market, growing at 20.5 per cent annually.

Aimia’s base of corporate partners for its traditional Aeroplan program gives the company another key advantage when pursuing this opportunity: all partners become potential participants in the Aeroplan Business program. Introducing Aeroplan Business to these companies would see the development of a complete points ecosystem, where businesses purchase Aeroplan points for their consumers while simultaneously earning and redeeming Aeroplan Business points. This new business program would increase Aeroplan’s revenue on two fronts: B2B customer purchases through the American Express corporate card and purchases made toward B2B partner products would effectively double Aimia’s revenues on a given transaction.

Increasing Thrust Through Dynamic Points

In addition to revamping the Aeroplan program, Aimia should further invest in its data analytics capabilities. The company holds a wealth of data on the purchasing habits of its five million end users who shop at accumulation partners such as Costco and Uniprix. This data is owned exclusively by Aimia and, as one of the company’s most important assets, should become a critical component of the company’s value proposition. Therefore, it is recommended that Aimia develop and integrate into its service offering, a proprietary dynamic pricing scheme using its Aeroplan points as currency.

While traditional dynamic pricing has successfully boosted many companies’ profits, it does not come without its downfalls. Its potential to frustrate customers has been well-documented, with Uber’s surge pricing being a notable example. The ideal form of dynamic pricing would shift consumer demand without increasing the price of a product and consequently angering customers.

This presents a business opportunity for Aimia. Aeroplan points are a form of currency to which consumers attach value: more purchases would be made if a product purchase came with 1,000 loyalty points as compared to 100. However, consumers pay for the transaction in cash, not points, and the point inflow is perceived as a bonus. Like changing the price of a good, altering the number of points associated with a purchase would have an impact on aggregate consumer demand, but consumers would be significantly less upset than if prices were to be raised.

Aimia is particularly well-positioned to venture into dynamic pricing of points: it has access to reams of data on consumer purchasing habits from Aeroplan. From a strategic perspective, doing so is crucial, as it increases the value Aimia offers to its partners and decreases the likelihood that firms will abandon Aimia as Air Canada did.

Full Spead Ahead

Aeroplan’s renewed strategy will provide a much-needed boost to the firm’s revenues going forward. Assuming Aimia captures four per cent of the serviceable market in the first year, business customers would earn Aeroplan points on C$234-million-worth of purchases made through Aeroplan’s corporate business cards, including travel-related services, food delivery products, and educational programs. Approximately C$15 million will be generated through the sale of Aeroplan points on additional product and service purchases. Another C$9 million would be generated on travel management fees earned through the Aeroplan Travel Management program, using a three-per- cent capture rate in the first year. As both B2B customers and partners increase, the gross billings and travel management fees collected by Aimia will increase annually on a per-client basis. Assuming Aeroplan’s B2B business can achieve a similar level of success as its business-to-consumer (B2C) offering, Aeroplan can expect to generate C$242 million in gross billings 10 years after its departure from Air Canada purely from these new business lines.

Aimia’s historical overdependence on Air Canada was a significant strategic misstep. Moving forward, Aeroplan must leverage its strong brand and rebuild its network. A short-term focus on B2C consumer retention combined with a long-term expansion of the program’s B2B business will ensure the company mitigates any immediate damage and positions itself well for future growth. Offering dynamic pricing of Aeroplan points as a complement to its business will provide additional value to Aeroplan partners, distinguishing the company from its competitors and increasing the likelihood that partners will choose to remain with the company. While this contract cancellation has obviously dealt a significant blow to the company, there may be a silver lining: it might finally be the impetus Aimia needs to step out of Air Canada’s shadow and become a major company in its own right.