SpaceX : The Big Falcon Problem

By: Bianca Miele and Cameron Hands

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

The Journey to Mars

Since 1993, NASA’s funding has been steadily decreasing following the end of the Cold War era space race, and is now less than 0.5 per cent of the federal budget. After the Commercial Space Launch Amendments Act legalized the privatization of space travel in 2004, many private companies moved to fill the void left by NASA’s discontinued operations. With rapid industry growth, investments have flooded into commercial space startups. Venture capital firms invested $1.8 billion in 2015, doubling the cumulative amount of venture funds invested in the previous 15 years.

Space Exploration Technologies Corp. (SpaceX), one of the industry’s pioneers, was founded in 2002 by Elon Musk, who is still currently serving as the CEO and Lead Designer. The California-based company was founded on the overarching goal of making humankind an interplanetary species. SpaceX is aiming to start its mission to Mars by the year 2022. Although rich in venture capital, the company requires billions more to complete the development of its next-generation interplanetary launch system to colonize Mars.

SpaceX Needs Cash

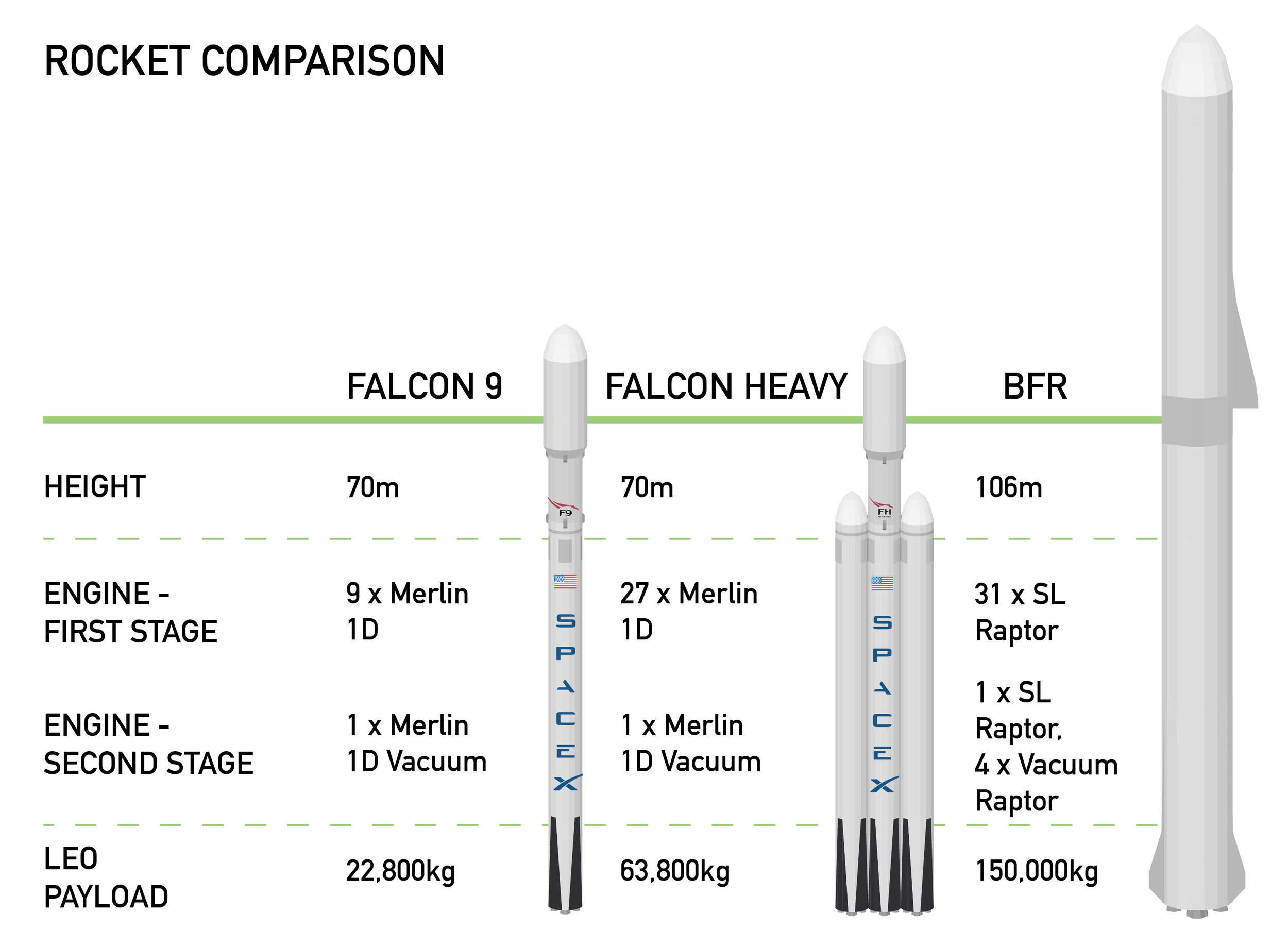

In Musk’s recent presentation on colonizing Mars he revealed that SpaceX is in the process of developing a next-generation launch vehicle codenamed Big Falcon Rocket (BFR). The BFR is a multipurpose system intended to replace the Mars launch duties of the Interplanetary Transport System (ITS) with an estimated development cost of $10 billion.

To fund projects, SpaceX has historically relied on equity financing. Following a $351 million Series H round of funding in July 2017, SpaceX is now worth approximately $21.2 billion, making it one of the most valuable privately held corporations in the world. Only six other venture-backed companies are worth $20 billion or more. However, SpaceX cannot continue to rely on equity financing to fund the company.

To date, many investors have invested in Musk due to a belief in his long-term plans and ambitious mission statements. In other words, Tesla’s mission to create a mass market for electric cars and Solar City’s plan to accelerate society’s transition to sustainable energy. This belief is unsustainable, as the failure of one of Musk’s companies destroys the credibility of his promises and subsequently, his ability to raise future capital. Tesla Motors, Musk’s most mainstream venture, has been frequently criticized for its high cash burn rate. As a result, Tesla has been pursuing alternative sources of financing, such as requiring hefty deposits on orders to help fund the company through its production challenges. Like Tesla, SpaceX will need to find other internal methods of generating cash flow moving forward.

A Five Billion Dollar Black Hole

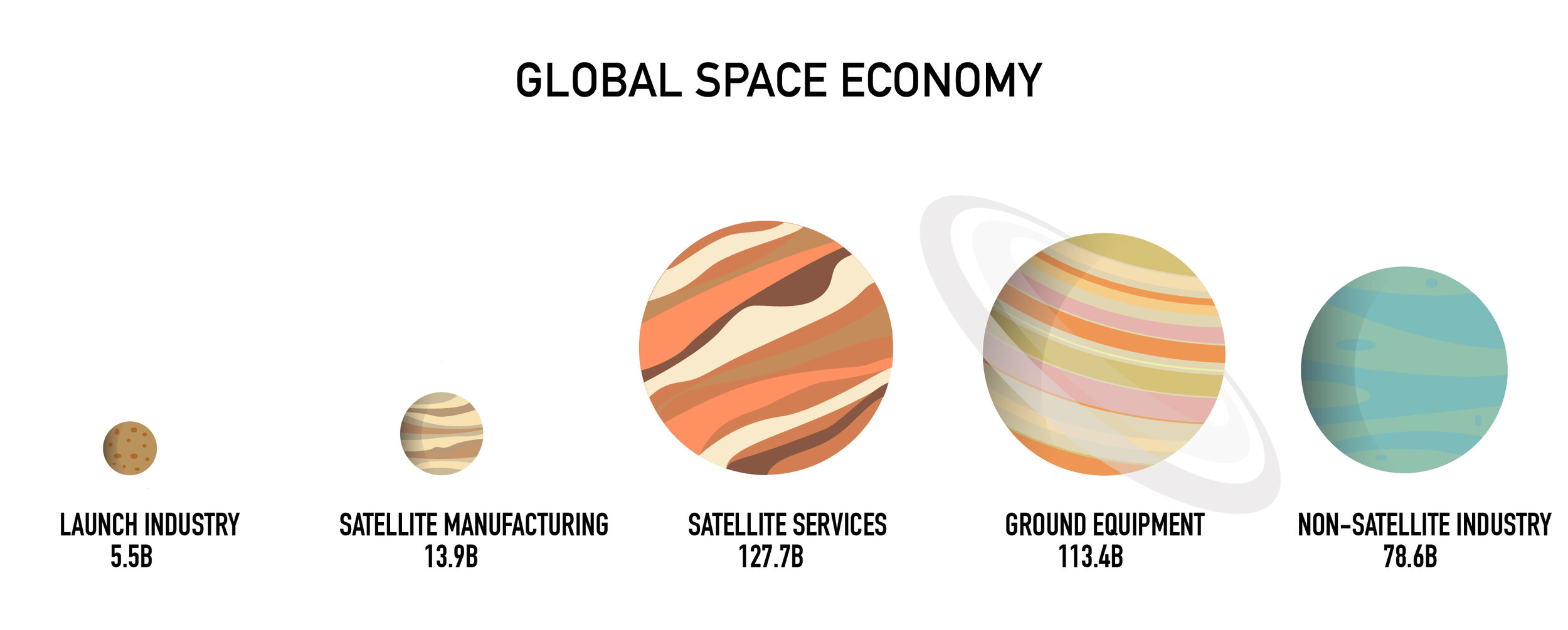

Currently, SpaceX solely operates in the rocket launch segment of the space industry. According to a Bryce Space and Technology study, this makes SpaceX only privy to approximately $5.5 billion of the total $339-billion space market. This is 1.6 per cent of the total annual revenues generated by the space industry, which is dominated by satellite companies. The quantity and frequency of rocket launches depend on the activity of outside entities such as governments, militaries, and companies reliant on the deployment of satellites.

Companies operating within the rocket launch industry are differentiated based on pricing and their launch capabilities. SpaceX is differentiating itself from other competitors, such as the United Launch Alliance (ULA), by undercutting their costs. This is accomplished through backwards integration, in which more than 70 per cent of manufacturing is done in-house. In addition, SpaceX parts have reduced costs by around 40 per cent versus competitors, a reduction attributed to the practice of reusing rockets and other expensive components.

SpaceX currently offers two multi-staged rocket systems. The Falcon 9 can deliver a payload with a maximum weight of 18,300 pounds to a geosynchronous transfer orbit (GTO); reaching this level of elevation is essential for many types of satellites, such as those needed for television and radio broadcasting and communications. The Falcon Heavy has significantly more thrust and can deliver 58,860 pounds to a GTO. Assuming a 2018 launch window and a “standard payment plan”, SpaceX charges $62 million and $90 million respectively per launch.

Based on these launch prices, there is a gap between the level of cash that can be generated and the cash SpaceX needs. Assuming an average launch cost of $62 million to be conservative, a target rate of one launch per week, and a generous 40-per-cent margin, SpaceX will net a little less than $5.2 billion from 2018 to 2021. This suggests a shortfall of approximately $5 billion, assuming the $10-billion development cost for the BFR. The company will most likely not lower costs below $62 million as no other competitor has come close to threatening SpaceX’s position as a cost leader.

Houston, We Have a Problem

Due to the hyper-competitive launch industry and the $5-billion funding gap, SpaceX must find another source of revenue to foot its multibillion-dollar bill for developing the BFR. To do this, SpaceX plans to launch 4,425 interconnected satellites by 2025 to provide global broadband Internet. However, there are three reasons why this strategy is insufficient: the aggressive 4,425 launch schedule is operationally unrealistic, the overall increase in advanced pure-play competition will drive down SpaceX’s market share, and the satellite broadband industry generates a mere $2.0 billion in annual revenue.

First, this operation would require a record number of annual launches within tight windows, something that SpaceX has been unable to do thus far. In terms of a cost breakdown, each satellite weighs around 386 kilograms and the entire project is expected to cost $10 billion. With a payload of approximately 11,000 pounds per Falcon 9 launch, SpaceX would need at least 302 launches with 14 satellites per launch to reach its goal of 4,425 satellites by 2025; this equates to roughly 43 launches annually. This aggressive launch schedule far surpasses SpaceX’s current performance metrics with only 15 Falcon 9 launches this year as of October 2017. Second, advanced competitors already exist in the satellite Internet market. OneWeb Ltd, a global communications company, has already secured the necessary rights to international radio frequencies needed to deliver high-speed Internet signals. OneWeb has raised $1.7 billion of venture capital to build and deploy their “constellation” of 648 satellites and construct its factory opening next year, which is capable of building 15 satellites per week, a record for the industry. Its constellation will launch in three batches and broadband service is expected to be available to consumers by 2019, one year before SpaceX. OneWeb has projected that by 2025 it will support one billion consumers worldwide. Lastly, this $2.0 billion global satellite industry grew by a modest two per cent in 2016, which was below worldwide economic growth of 3.1 per cent. This means that for SpaceX to fill in the $5-billion gap, the satellite broadband industry must not only grow 400 per cent by 2025, but SpaceX must also achieve an unrealistic 100-per-cent market share.

In sum, an aggressive and unprecedented launch schedule, a growing number of advanced competitors, and the small $2-billion satellite broadband industry will make it incredibly difficult for SpaceX to fill the $5-billion gap to fund the BFR. As such, Musk must develop alternative cash-flow generating strategies to complement SpaceX’s current satellite launch strategy to achieve his goal of colonizing Mars by 2022.

An Advantage in a Competitive Space

SpaceX has become competitive in the rocket launch industry by adopting a cost-leader strategy since its incorporation in 2002. SpaceX can afford to offer significantly lower prices than its competitors due to the reusability of SpaceX components. Historically, rockets were not designed to be reusable as many components would either not survive the fall back to Earth, or would be abandoned after they had plummeted into the ocean. Following years of research and billions of dollars spent on development, SpaceX is leading the reusability race. Musk has stated that the first stage of a Falcon 9 is designed to be launched 10 successive times before any hardware replacements are necessary, and 100 times before moderate refurbishment is necessary.

Naturally, because of the significant cost savings involved with reusability, some competitors are beginning to make small investments in next-generation launch systems. That is to say, systems which aim to be less expensive, more reliable, and have increased levels of reusability. For example, the ULA has secured $201 million in funding from the U.S. Air Force in addition to that secured from private sources to develop “Vulcan”, a two-stage-to-orbit (TSTO), heavy-payload rocket similar to Falcon Heavy. Like SpaceX’s current portfolio of launch vehicles, ULA is designing Vulcan to be reusable. ULA believes that the Vulcan’s first flight will occur sometime in 2019 and that the base cost for a launch will cost $99 million.

There are two key advantages to SpaceX’s reusable rockets. First, SpaceX’s reusable Falcon 9 rockets, priced at $61.2 million per launch, are sufficiently cheaper than competitors. This is mainly due to expertise in research and development (R&D) and manufacturing that falls in line with SpaceX’s cost leader strategy. Furthermore, SpaceX is the only company to publicly state plans to achieve second stage reuse. This means recovering the upper engine of rockets, which is a harder technical challenge than recovering the first stage or lower engine.

As such, SpaceX’s expertise in reusability both financially and technically positions the company to generate revenues through either selling parts or providing services to increase reusable rocket launch efficacy. An analogous industry where this strategy has been applied to is the mobile phone landscape. As the industry moves towards organic light-emitting diode (OLED) screens for edge-to-edge displays, demand is increasing for suppliers of OLED technology. Samsung, the clear leader in producing OLED screens, acts as the sole supplier to build Apple’s iPhone 8.

Rocketing Towards Supply Chain Commercialization

SpaceX can commercialize parts of its supply chain to satisfy the $5-billion funding gap of the BFR development. SpaceX can leverage its capabilities in manufacturing, and R&D to outsource reusable components to other space companies launching rockets. Reusable rockets have a clear advantage in this industry, and other competitors are increasing investments into designing reusable parts leading to their compatibility with SpaceX parts. This initiative also aligns with SpaceX’s mandate of promoting space innovation to reach Mars.

The major cost components of any rocket include the first-stage engine, second-stage engine, and rocket boosters. The average cost of these components in the industry is $68 million for a one-time launch. Conversely, SpaceX can sell the same components for $39 million at a 40-per-cent margin for 10 launches before replacement is required. Evidently, procuring reusable parts provides significant cost savings for SpaceX consumers.

In addition, to make these components compatible with its customers’ rocket designs and to provide the services required to operate these parts, SpaceX can incorporate a $40-million service fee into their sales. This service fee includes all the necessary assistance needed from SpaceX to ensure successful launches. This brings the total “package” cost to procure SpaceX components to $79 million for parts that can be reused up to 10 times. After 10 rocket launches, a SpaceX customer will realize up to $590 million in savings.

At a 40-per-cent margin, SpaceX would need to sell 90 packages to generate the $5 billion in cash it needs. There are approximately 17 manufacturers of space rockets internationally in which major competitors have invested into reusable components, and 134 scheduled launches for 2018. Initially, sales will be limited to manufacturers who currently have the capabilities to incorporate reusable engines into their rockets. However, supplying SpaceX engines in the market should lower the technical barriers for other manufacturers to begin developing the necessary reusable components to also become SpaceX customers. With its superior reusable technology and significant cost savings, it is reasonable to expect SpaceX to achieve this target in time for the BFR deadline.

Conveniently, acting as a supplier within this industry already has precedent. Aerojet Rocketdyne, a public company operating in the defence and aerospace industry, develops and manufactures several types of propulsion systems for rockets and missiles. Aerojet sells as a prime contractor or a subcontractor on a project-by-project basis. One of the company’s largest customers is ULA, which currently uses Aerojet Rocketdyne engines for Delta-IV launches.

One Team, One Dream

SpaceX is different from most multi-billion-dollar companies. It operates in a brand-new industry that is incredibly complex and may be out of reach for many investors. To depend less heavily on equity investors, and to increase its operational financial stability, SpaceX should behave in a more orthodox manner. By commercializing parts of its supply chain, SpaceX will be able to close the $5 billion BFR funding gap through the sale of reusable products and services to strengthen success rates of launches.

Although it may seem counterintuitive to help competitors who are operating in the same industry, the race to Mars is not purely a business opportunity, but also a societal one. Musk has always believed that colonizing Mars will save humanity and that commercialization is an integral catalyst toward this goal. Given Musk’s past open-sourcing of Tesla patents and belief in free market ideas, the adoption of the commercialization strategy by SpaceX is realistic. After all, it was Musk who emphatically stated that the goal of Tesla Motors is to “accelerate the advent of sustainable transport by bringing compelling mass market electric cars to market as soon as possible.”